Introduction

Section 9(1) of the Central Goods and Services Tax Act, 2017 (“CGST Act”) is the principal charging provision governing the levy and collection of tax.

Like every fiscal statute, GST derives its enforceability not merely from the existence of taxable transactions but from a valid charging section enacted under constitutional authority. While Section 7 defines the scope of “supply”, Section 9(1) imposes the tax.

Consequently, no liability can arise merely because an activity qualifies as a supply unless it is also brought within the charging mechanism of Section 9.

The significance of Section 9(1) has increased considerably with developments such as the exclusion of Extra Neutral Alcohol (ENA), disputes relating to petroleum products, reverse charge provisions, classification controversies, and the growing body of GST jurisprudence interpreting the concept of levy.

This article analyses Section 9(1) from constitutional and legislative history perspectives.

Constitutional Foundation of Section 9

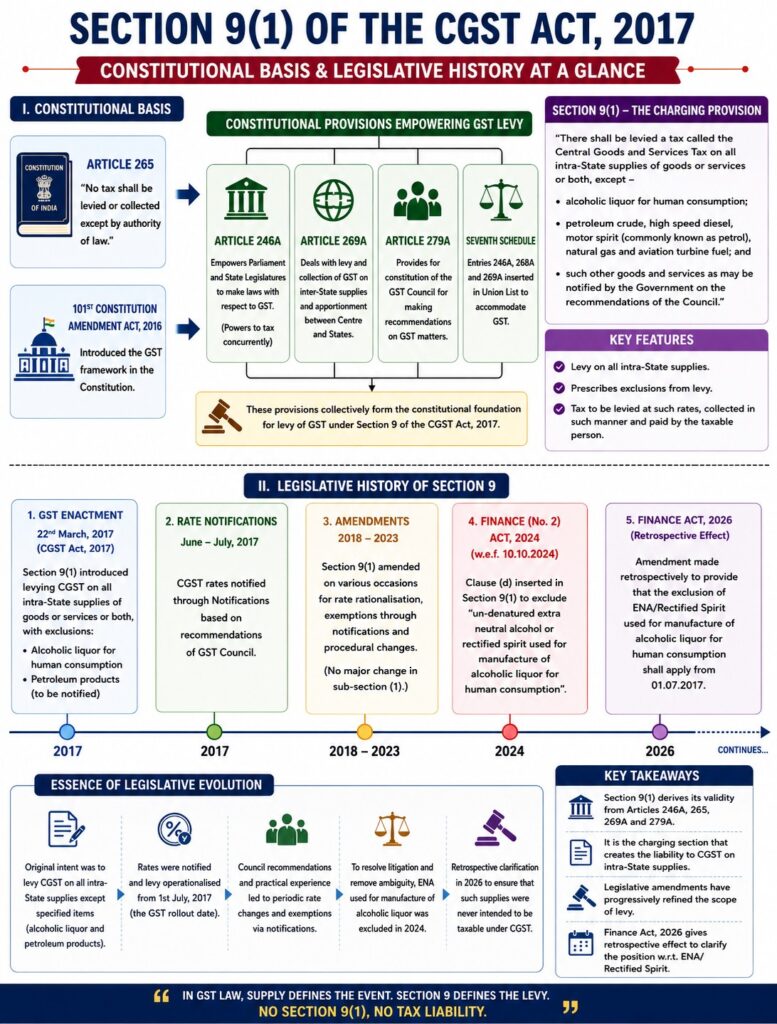

Article 265 of the Constitution provides:

“No tax shall be levied or collected except by authority of law.”

This principle constitutes the foundation of all taxation statutes in India.

The Supreme Court has consistently held that taxation cannot arise through implication, inference, administrative practice, executive circulars, or equitable considerations.

For a valid levy, the following elements must exist:

- Taxable event

- Taxable person

- Measure of tax

- Rate of tax

Absence of any of these components renders the levy vulnerable to constitutional challenge.

Constitutional Basis of GST

GST derives its authority primarily from:

Article 246A

Introduced through the Constitution (101st Amendment) Act, 2016.

Article 246A confers concurrent powers upon Parliament and State Legislatures to enact GST laws.

This marked a departure from the traditional separation of taxing powers under the Seventh Schedule.

Article 269A

Provides for the levy and collection of GST on inter-State supplies.

Article 279A

Provides for constitution of the GST Council.

Position Prior to GST

Prior to GST:

- Central Excise was levied on manufacture.

- Service Tax was levied on provision of services.

- VAT/CST was levied on sale of goods.

Each levy had a separate charging provision.

GST replaced multiple taxable events with a single taxable event:

Supply

However, despite this conceptual shift, the constitutional requirement of a charging section remained unchanged.

Legislative History of Section 9

Section 9 originally provided:

There shall be levied a tax called Central Goods and Services Tax on all intra-State supplies of goods or services or both except alcoholic liquor for human consumption.

Thus, from inception:

Excluded Supplies

- Alcoholic liquor for human consumption

- Petroleum products (temporarily kept outside levy until notified)

Finance Act (No. 2) Act, 2024

A significant amendment was inserted:

“and un-denatured extra neutral alcohol or rectified spirit used for the manufacture of alcoholic liquor for human consumption” Consequently, ENA used for the manufacture of potable alcohol was excluded from the GST levy.

Finance Act, 2026

The Finance Act, 2026, further clarified and retrospectively regularised the position relating to ENA supplied for the manufacture of alcoholic liquor for human consumption.

The amendment effectively recognised that GST was never intended to apply to such supplies.

The legislative objective was to resolve longstanding disputes arising from divergent practices adopted across States.

Conclusion

Concluding Remarks to Chapters 1 and 2

The constitutional and legislative journey of Section 9(1) reveals that it is far more than a mere charging provision; it is the statutory embodiment of India’s GST architecture.

The authority to levy GST originates from the constitutional framework comprising Articles 246A, 265, 269A and 279A, while Section 9(1) serves as the legislative instrument through which that constitutional power is exercised.

The principle that no tax can be levied or collected except by authority of law remains the cornerstone of GST jurisprudence and underscores the centrality of Section 9(1) in determining tax liability.

We then traced the evolution of Section 9(1) from its inception on 1 July 2017 to its subsequent refinements through legislative amendments, notifications, and policy interventions. The legislative history demonstrates that GST is not a static tax but a continuously evolving framework responding to economic realities, judicial developments and stakeholder concerns.

The exclusion of alcoholic liquor for human consumption, the deferred inclusion of petroleum products, and the subsequent treatment of Extra Neutral Alcohol (ENA) and rectified spirit illustrate how Parliament has repeatedly revisited the scope of the levy to ensure alignment with constitutional principles and fiscal policy objectives.

The retrospective amendments relating to ENA represent perhaps the most significant refinement of the charging provision since the introduction of GST, reaffirming that the contours of taxability are ultimately determined by the scope of the levy itself and not merely by the breadth of the definition of supply.

Viewed together, Section 7 creates the taxable event, but Section 9 creates the tax. A transaction may constitute a supply, yet remain outside GST if Parliament chooses not to levy tax upon it.

Consequently, every enquiry into GST liability must begin with an examination of the charging provision before proceeding to questions of classification, valuation, exemptions, place of supply, or input tax credit.

This approach is consistent with settled principles of fiscal jurisprudence and the structure of the CGST Act itself, where “Levy and Collection of Tax” immediately follows the provisions dealing with “Scope of Supply”.

The legislative arrangement is deliberate and reflects the fundamental legal principle that a tax cannot exist in the absence of a valid charge. The CGST Act accordingly places Section 9 at the heart of the GST framework within Chapter III dealing with Levy and Collection of Tax.

In the next article, the focus will shift from the source of legislative power and the history of amendments to the individual components of the charging provision itself—namely the concepts of levy, taxable person, intra-State supply, value, rate and collection.

It is only through a careful examination of these constituent elements that the true scope and operation of GST can be understood. This will seek to answer the central question that lies at the core of every GST dispute:

Before asking whether a supply is taxable, one must first ask whether there is a valid levy under Section 9(1).

Leave a Reply