Introduction

Section 8 of the Central Goods and Services Tax Act, 2017 prescribes the manner in which tax liability is determined in cases involving composite and mixed supply.

While Section 7 determines whether a transaction constitutes a supply, Section 8 determines the tax treatment applicable where multiple goods and/or services are supplied together.

The provision seeks to address a fundamental challenge arising in modern commercial transactions where a single supply package frequently comprises multiple elements.

Such transactions often involve a combination of goods and services, each of which may attract different tax rates if supplied independently. In the absence of a specific provision, classification disputes could result in uncertainty regarding the applicable tax rate.

To address this issue, the GST law introduced two distinct concepts:

- Composite Supply [Section 2(30)]

- Mixed Supply [Section 2(74)]

Section 8 provides the mechanism for determining the tax liability applicable to these supplies.

In the case of a composite supply, tax liability is determined based on the principal supply, whereas in the case of a mixed supply, tax liability is determined based on the supply attracting the highest rate of tax.

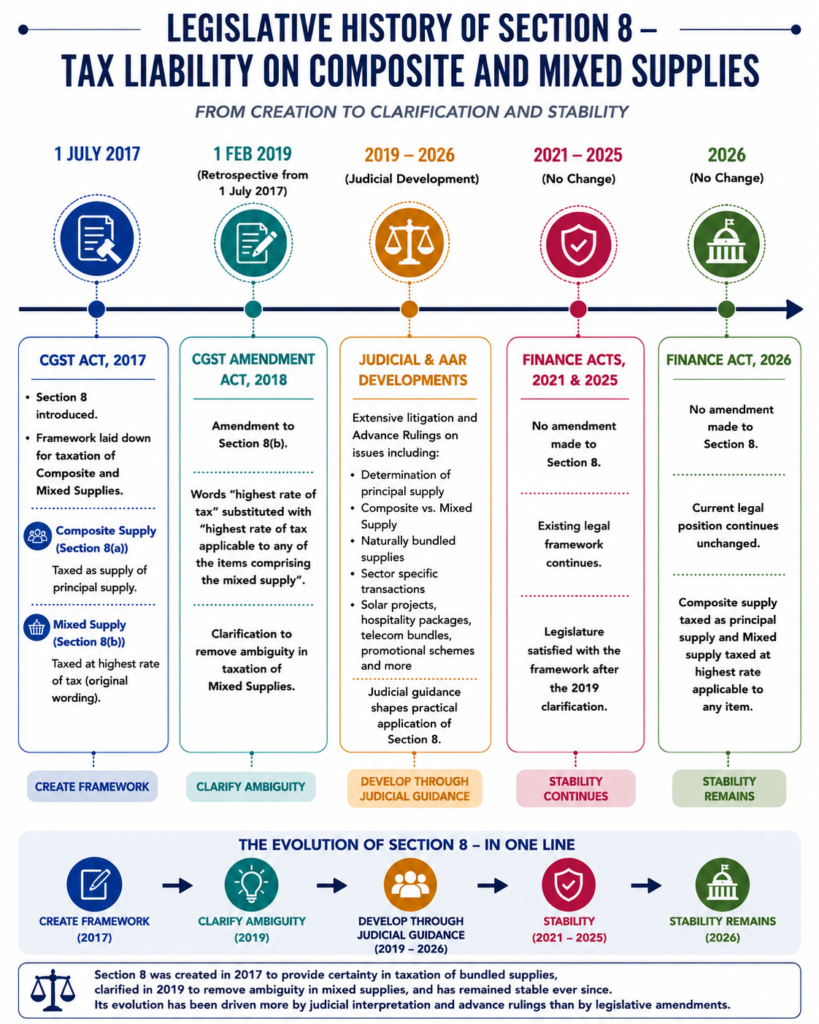

The legislative history of Section 8 differs significantly from that of Section 7. While Section 7 witnessed substantial amendments affecting the scope of supply itself, Section 8 has remained largely stable since its introduction.

The only substantive statutory amendment was introduced through the CGST (Amendment) Act, 2018, which clarified the methodology for determining tax liability in respect of mixed supplies. Thereafter, no amendments were made through the Finance Acts of 2021, 2025 or 2026.

Notwithstanding the limited legislative amendments, Section 8 has generated significant litigation relating to:

- Determination of principal supply;

- Naturally bundled supplies;

- Composite supply versus mixed supply;

- Solar power projects;

- EPC contracts;

- Hospitality and tourism packages;

- Promotional schemes and bundled offers;

- Telecom and digital service bundles.

Consequently, the evolution of Section 8 has been driven primarily by judicial pronouncements, advance rulings and departmental clarifications rather than legislative intervention.

Composite and Mixed Supply – Legislative and Judicial Developments (2017–2026)

Click here for the table that traces the complete legislative evolution of Section 8 from its inception on 1 July 2017 until the Finance Act, 2026, highlighting the statutory amendments, policy rationale, judicial triggers, compliance implications, revenue impact and practical consequences for taxpayers and consumers.

Important Circulars Impacting Section 8

Although no circular specifically amended Section 8, several circulars have influenced interpretation of composite and mixed supply:

| Circular No. | Subject | Relevance to Section 8 |

|---|---|---|

| 11/11/2017-GST dated 20.10.2017 | Printing contracts | Principal supply determination |

| 34/8/2018-GST dated 01.03.2018 | Bus body building | Composite supply analysis |

| 177/09/2022-TRU dated 03.08.2022 | GST Council clarifications | Bundled supply and classification issues |

Landmark Judicial Developments

| Case Law | Principle Established |

|---|---|

| Abbott Healthcare Pvt. Ltd. | Determination of principal supply in bundled transactions |

| Torrent Power Ltd. | Naturally bundled supplies and principal supply test |

| Switching AVO Electro Power Ltd. | Distinction between composite and mixed supply |

| Kalyan Jewellers India Ltd. | Ancillary supplies follow principal supply. Note that this is no longer applicable as per the latest amendment, where vouchers are no longer taxable. |

| Premier Sales Promotion Pvt. Ltd. | Tax treatment of promotional packages. Note that this is no longer applicable as per the latest amendment, where vouchers are no longer taxable. |

| Solar EPC Project rulings | Composite supply versus works contract disputes |

| Telecom bundle rulings | Bundled supply analysis in digital economy |

Major Legislative Milestones

| Period | Position |

|---|---|

| 01.07.2017 – 31.01.2019 | Original Section 8 governing composite and mixed supply |

| 01.02.2019 onwards | Clarificatory amendment to Section 8(b) regarding highest rate in mixed supplies |

| 2019–2026 | No further amendments; development through litigation and rulings |

Top Issues under Section 8

| Rank | Issue |

|---|---|

| 1 | Composite supply vs mixed supply |

| 2 | Identification of principal supply |

| 3 | Naturally bundled services |

| 4 | Solar power projects |

| 5 | Hospitality and tourism packages |

| 6 | Promotional schemes and bundled offerings |

Overall Ratings

| Parameter | Assessment |

|---|---|

| Revenue Sensitivity | High |

| Compliance Sensitivity | Medium |

| Litigation Sensitivity | Very High |

| Frequency of Amendments | Very Low |

| Judicial Influence | Very High |

| Current Stability | High |

Conclusion – Composite and Mixed Supply

Section 8 represents one of the most important interpretational provisions under the GST regime. While Section 7 determines whether a transaction constitutes a supply, Section 8 determines the tax treatment applicable where multiple supplies are bundled together. The provision therefore acts as a bridge between classification and taxation.

Unlike many other GST provisions, the legislative evolution of Section 8 has been remarkably limited.

Since its introduction on 1 July 2017, only one substantive amendment has been made through the CGST (Amendment) Act, 2018, which clarified the methodology for determining tax liability in mixed supplies. Thereafter, the Legislature has largely allowed the provision to evolve through judicial interpretation and administrative guidance.

The jurisprudence surrounding Section 8 demonstrates that the principal challenge is not legislative uncertainty but factual determination. Questions such as whether supplies are naturally bundled, whether a principal supply exists, and whether a transaction constitutes a composite supply or a mixed supply continue to generate significant litigation.

Consequently, courts, advance ruling authorities and appellate authorities have played a pivotal role in shaping the practical application of the provision.

As of the Finance Act, 2026, Section 8 remains substantially unchanged from the framework established in 2019. The provision has therefore entered a phase of legislative stability, although evolving business models, digital offerings, bundled services and innovative commercial arrangements will continue to test its boundaries.

In essence, the legislative history of Section 8 may be summarised in three words:

Creation (2017) → Clarification (2019) → Stability (2026).

Leave a Reply