Introduction

Section 7 of the Central Goods and Services Tax Act, 2017 is the cornerstone of the GST framework, as it defines the expression “supply”, which constitutes the taxable event under the GST regime. Unlike the pre-GST indirect tax structure where distinct taxable events such as manufacture, sale, provision of service, entry of goods into a local area, or purchase of goods triggered tax liability, GST seeks to levy tax on a single unified taxable event, namely supply of goods or services or both.

The importance of Section 7 stems from the fact that no transaction can be subjected to GST unless it first qualifies as a “supply” within the meaning of this provision. Consequently, determination of taxability under GST invariably begins with an examination of Section 7. The provision not only identifies transactions that constitute supply but also excludes certain activities from its ambit through Schedule III and empowers the Government to notify specified transactions for classification purposes.

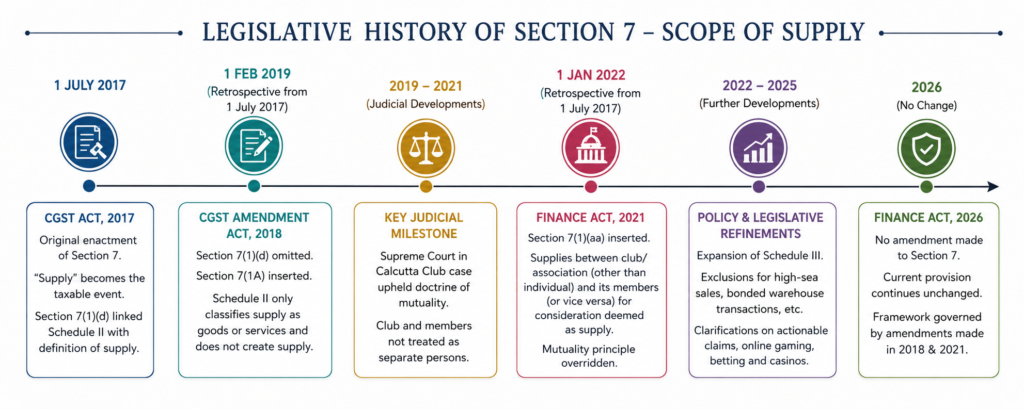

At the time of introduction of GST on 1 July 2017, Section 7 was designed as an inclusive definition encompassing all forms of supply such as sale, transfer, barter, exchange, licence, rental, lease and disposal undertaken for consideration in the course or furtherance of business. However, practical implementation of GST gave rise to several interpretational challenges regarding:

- The relationship between Section 7 and Schedule II;

- Taxability of transactions between clubs/associations and their members;

- Scope of activities undertaken without consideration;

- Treatment of import-related transactions;

- Application of the doctrine of mutuality;

- Taxability of actionable claims and emerging digital business models.

As a result, Section 7 has evolved significantly through legislative amendments, judicial pronouncements and administrative clarifications. While the number of statutory amendments to the provision has been relatively limited, their impact has been far-reaching. In particular, the CGST (Amendment) Act, 2018 fundamentally altered the role of Schedule II by introducing Section 7(1A), whereas the Finance Act, 2021 inserted Section 7(1)(aa) to legislatively override the Supreme Court’s decision in State of West Bengal v. Calcutta Club Ltd. and bring supplies between clubs and their members within the GST net.

From a policy perspective, the evolution of Section 7 demonstrates a continuous effort by the Legislature to balance three competing objectives:

- Widening and protecting the tax base;

- Providing certainty in the determination of taxable supplies; and

- Reducing litigation arising from interpretational ambiguities.

The legislative journey of Section 7 may broadly be divided into three phases:

| Phase | Period | Key Characteristics |

|---|---|---|

| Phase I | 01.07.2017 to 31.01.2019 | Original framework where Schedule II was linked directly with the definition of supply through Section 7(1)(d). |

| Phase II | 01.02.2019 to 31.12.2021 | Introduction of Section 7(1A) through the CGST (Amendment) Act, 2018, clarifying that Schedule II merely classifies a supply and does not independently create one. |

| Phase III | 01.01.2022 onwards | Introduction of Section 7(1)(aa) through the Finance Act, 2021, deeming clubs/associations and their members as separate persons and overriding the doctrine of mutuality. |

Notably, despite several amendments being made to the CGST Act through subsequent Finance Acts, including the Finance Act, 2026, no further amendment has been made to Section 7 after the changes introduced by the Finance Act, 2021. Accordingly, the present legal framework governing the concept of supply continues to be based substantially on the amendments introduced in 2018 and 2021.

Click here for the table that traces the complete legislative evolution of Section 7 from its inception on 1 July 2017 until the Finance Act, 2026, highlighting the statutory amendments, policy rationale, judicial triggers, compliance implications, revenue impact and practical consequences for taxpayers and consumers.

Top Three Amendments by Importance

| Rank | Amendment | Significance |

|---|---|---|

| 1 | Section 7(1)(aa) – Finance Act 2021 | Overrode Calcutta Club and expanded tax base substantially. |

| 2 | Section 7(1A) – CGST Amendment Act 2018 | Clarified that Schedule II cannot independently create a supply. |

| 3 | Schedule III expansions | Eliminated double taxation on import-linked transactions. |

Overall Ratings for Section 7 Evolution

| Parameter | Assessment |

|---|---|

| Revenue Sensitivity | Very High |

| Compliance Sensitivity | High |

| Litigation Sensitivity | Very High |

| Frequency of Amendments | Low |

| Judicial Influence on Amendments | Very High |

| Current Stability of Provision | High (post Finance Act 2026) |

Conclusion

In conclusion, the legislative history of Section 7 reflects the gradual maturation of the GST regime. The provision has evolved from a broadly drafted charging concept into a more refined and judicially tested framework capable of addressing complex commercial transactions. Given its foundational role in determining taxability under GST, Section 7 will continue to remain one of the most significant and closely scrutinised provisions of the CGST Act, making a thorough understanding of its evolution indispensable for tax professionals, administrators, businesses and policymakers alike.

Leave a Reply