Before understanding how GST functions, it is essential to understand how the Constitution distributes taxation powers in India.

India follows a quasi-federal structure with a strong Centre, and the power to levy taxes is constitutionally divided between:

- Parliament (Union Government)

- State Legislatures

This distribution is primarily governed by Article 246 of the Constitution read with Schedule VII.

Article 246 – Distribution of Legislative Powers

Article 246 lays down who can legislate on what subject.

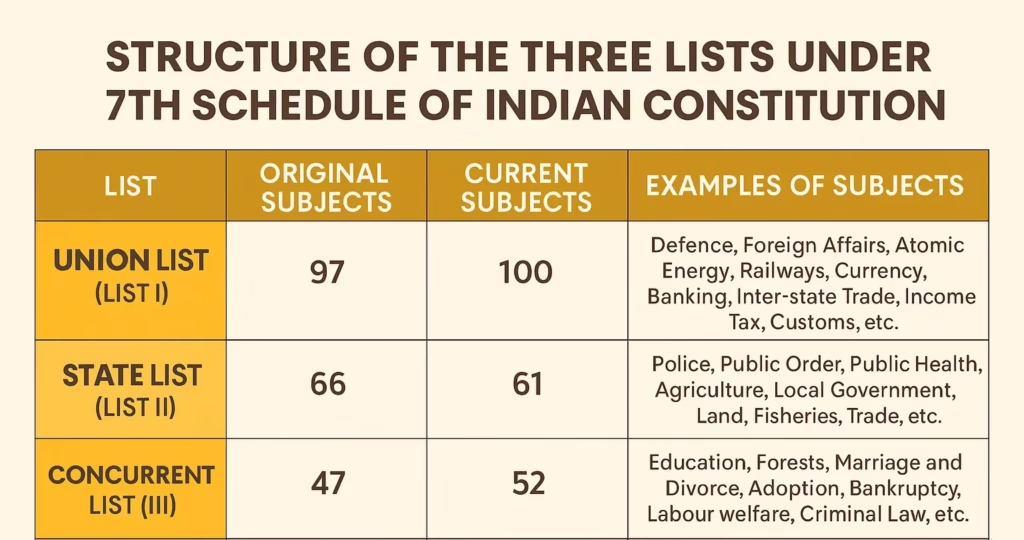

The Constitution divides subjects into three lists under Schedule VII:

1️⃣ List I – Union List

- Exclusive power of Parliament

- States cannot legislate on these matters

2️⃣ List II – State List

- Exclusive power of State Legislatures

- Parliament cannot legislate (except in exceptional circumstances)

3️⃣ List III – Concurrent List

- Both Parliament and State Legislatures can legislate

- Subject to the rule of repugnancy (explained later)

Understanding the Three Lists – A Simplified View

| List | Who Can Legislate? | Nature of Power |

|---|---|---|

| List I (Union List) | Parliament only | Exclusive |

| List II (State List) | State Legislatures only | Exclusive |

| List III (Concurrent List) | Both | Concurrent |

Examples of Tax Entries Before GST

🟢 Union List (List I)

Parliament had exclusive powers over:

- Central Excise Duty (on manufacture)

- Customs Duty

- Central Sales Tax (CST)

- Service Tax (through residuary power)

🔵 State List (List II)

States had exclusive powers over:

- Value Added Tax (VAT)

- Entry Tax

- Luxury Tax

- Tax on Advertisements

- Excise Duty on Alcohol

🟣 Concurrent List (List III)

- Both Centre and States could legislate on:

- Stamp Duty

- Certain aspects of SEZ laws

(Important: Taxation was largely not concurrent before GST. This becomes crucial later.)

Article 248 – Residuary Powers

What happens if a subject is not mentioned in any of the three lists?

That is where Article 248 comes into play.

Residuary Power = Parliament’s Exclusive Power

If a subject is:

- Not in List I

- Not in List II

- Not in List III

Then Parliament alone has the power to legislate.

This is supported by:

- Article 248

- Entry 97 of Union List

Classic Example: Service Tax

From 1994 to 2017:

- Service tax was levied under Entry 97 (Residuary Entry)

- Though Entry 92C (tax on services) was inserted, it was never operationalised

- Therefore, service tax survived purely on residuary powers

Article 254 – Doctrine of Repugnancy

Now comes the conflict resolution mechanism.

When both Parliament and State Legislatures legislate on a matter in the Concurrent List, what happens if there is inconsistency?

Article 254 provides the answer.

Doctrine of Repugnancy

If:

- A State law conflicts with a Central law

- Both relate to Concurrent List subjects

👉 The Central law prevails

👉 The State law becomes void to the extent of inconsistency

Important Clarification

This applies only to Concurrent List matters, not Union or State List matters.

Visual Representation: Conflict Resolution

Concurrent List Matter

↓

State Law vs Central Law Conflict

↓

Article 254 Applies

↓

Central Law Prevails

↓

State Law Void (to the extent of conflict)

Both can operate simultaneously —

But in case of clash → Union has the upper hand.

Pre-GST Tax Structure: Fragmented Regime

Before GST, taxation powers were divided as follows:

| Centre | States |

|---|---|

| Excise on manufacture | VAT on sale |

| Service Tax | Entry Tax |

| Customs | Luxury Tax |

| CST | Entertainment Tax |

This led to:

- Cascading effect

- Multiple compliances

- Different VAT laws in each State

- Complex tax credit mechanisms

The GST Vision – “One Nation, One Tax”

GST was conceptualised with two major objectives:

1️⃣ Unified Tax System

- Subsuming multiple indirect taxes

- Creating seamless credit flow

- Removing cascading

2️⃣ Preserving Federal Structure

India is a quasi-federal nation.

- States cannot be deprived of taxation powers

- Centre cannot monopolise indirect taxation

- Both must have simultaneous authority

This required a constitutional restructuring.

The 101st Constitutional Amendment – A Structural Shift

The 101st Constitutional Amendment achieved something unprecedented:

- Created a concurrent taxing power on supply

- Allowed both Centre and States to tax the same transaction

- Introduced a new taxable event

What is GST? (Constitutional Definition)

GST was defined by inserting Article 366(12A).

“Goods and Services Tax” means any tax on supply of goods or services or both.

This marked a major conceptual shift.

The Shift in Taxable Event

| Pre-GST | Under GST |

|---|---|

| Manufacture | Supply |

| Sale | Supply |

| Provision of Service | Supply |

GST replaced:

- Manufacture-based taxation

- Sale-based taxation

- Service-based taxation

With a single taxable event → Supply

Why Constitutional Amendment Was Necessary?

Earlier:

- Excise = Centre

- VAT = States

- Service Tax = Centre

There was no mechanism allowing both to tax the same transaction simultaneously.

GST required:

- Concurrent taxing powers

- Unified taxable event

- Harmonised framework

This required amending:

- Article 246

- Inserting Article 246A

- Amending Article 269

- Introducing GST Council (Article 279A)

Conclusion

Understanding GST without understanding:

- Article 246

- Schedule VII

- Article 248

- Article 254

is incomplete.

GST is not merely a tax reform —

It is a constitutional re-engineering of India’s fiscal federalism.

It balances:

- Unity

- Federal autonomy

- Concurrent taxation power

- National uniformity

Leave a Reply